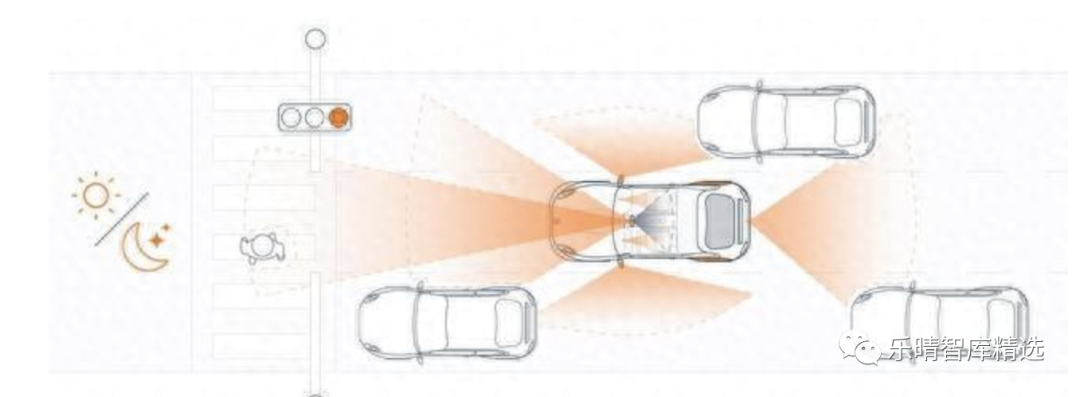

Recently, Ansome announced that its Hyperlux image sensor series products have been introduced into the NVIDIA DRIVE platform, which can greatly enhance the visual ability of autonomous vehicle and improve safety. With this combination of technologies, the auto drive system can take full advantage of the Hyperlux sensor and capture more details under any lighting conditions.

In the past, early unmanned vehicles mainly used LiDAR sensors, but in recent years, computer vision has developed rapidly, and low-cost visual sensing systems have also been widely used in the field of unmanned driving. Visual SLAM technology has pushed research to a new height and become an important research direction in the field of unmanned driving.

In addition, MetaAI previously released the basic model SegmentAnything Model (SAM) on its official website and made it open source. Its essence is to use GPT (based on the Transform model architecture) to enable computers to have the universal ability to understand individual "objects" in images.

The SAM model establishes a large-scale image segmentation model that can accept text prompts and obtain generalization ability through training on massive data.

Image segmentation is an important task in machine vision, which helps to identify and confirm different objects in the image, separate them from the background, and is particularly important in applications such as autonomous driving (detecting other cars, pedestrians, and obstacles) and medical imaging (extracting specific structures or potential lesions).

Machine vision is a rapidly developing branch of artificial intelligence.

According to CBInsight data, China is currently the third largest market for machine vision applications after the United States and Japan.

In terms of market size, as an emerging technology and industry, the Chinese machine vision industry is still relatively small in scale, but its growth rate is far faster than that of the world, and it is in a stage of rapid growth. GGII predicts that the market size of machine vision will exceed 120 billion yuan by 2025, and the industry has long-term and broad development prospects.

Machine vision panoramic structure diagram:

01. Overview of the Machine Vision Industry

According to the definition of machine vision by the Machine Vision Division of the Society of Manufacturing Engineers (SME) in the United States, machine vision is a device that automatically receives and processes an image of a real object through optical devices and non-contact sensors to obtain the required information or to control robot motion.

Machine vision is a collaboration between various fields such as artificial intelligence, computer science, image processing, and pattern recognition.

The technology of simulating human visual functions through computers, image sensors, and other related devices to endow machines with the ability to "see" and "recognize".

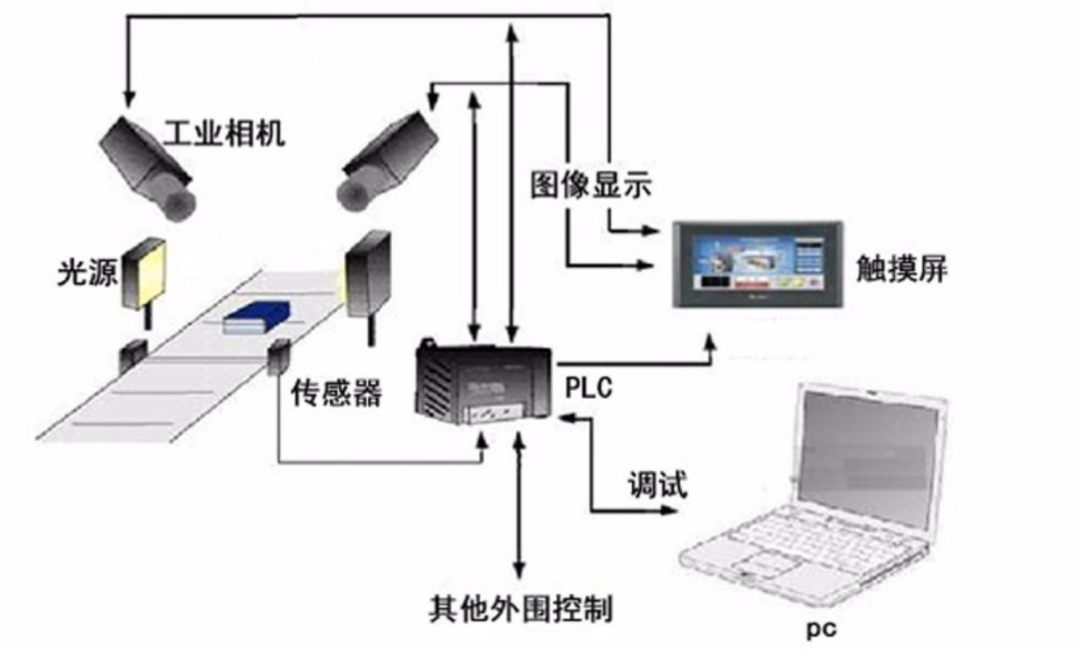

Machine vision equipment generally consists of two parts. 1) "Vision" refers to the hardware components of the system, mainly including: light source, lens, industrial camera, and image acquisition card; 2) "Jue" refers to the visual processing software of the system.

Machine vision includes four major functions: recognition, measurement, positioning, and detection, with detection technology being the most challenging.

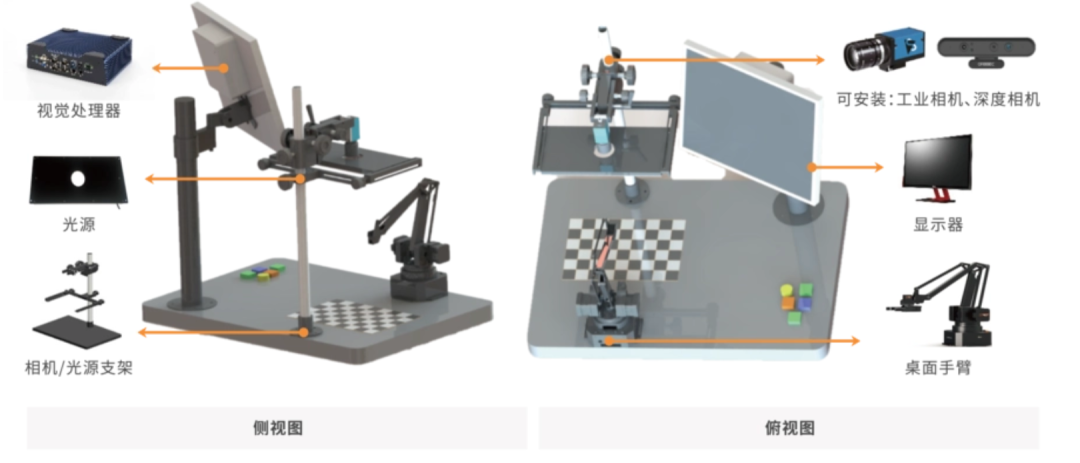

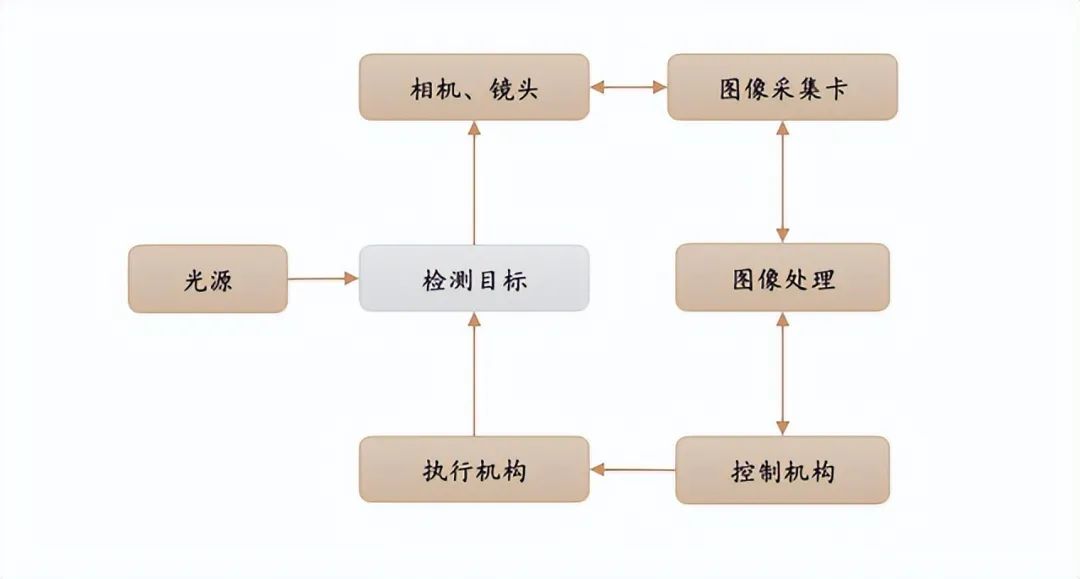

Machine vision workflow:

In the industrial field, machine vision has significant advantages over human vision.

Machine vision has advantages over artificial vision, such as high precision, fast speed, strong adaptability, high reliability, and high efficiency.

Against the backdrop of increased labor costs, digital transformation, and improved efficiency and quality requirements in the manufacturing industry in China, labor is gradually being replaced.

Comparison between machine vision and human eye vision:

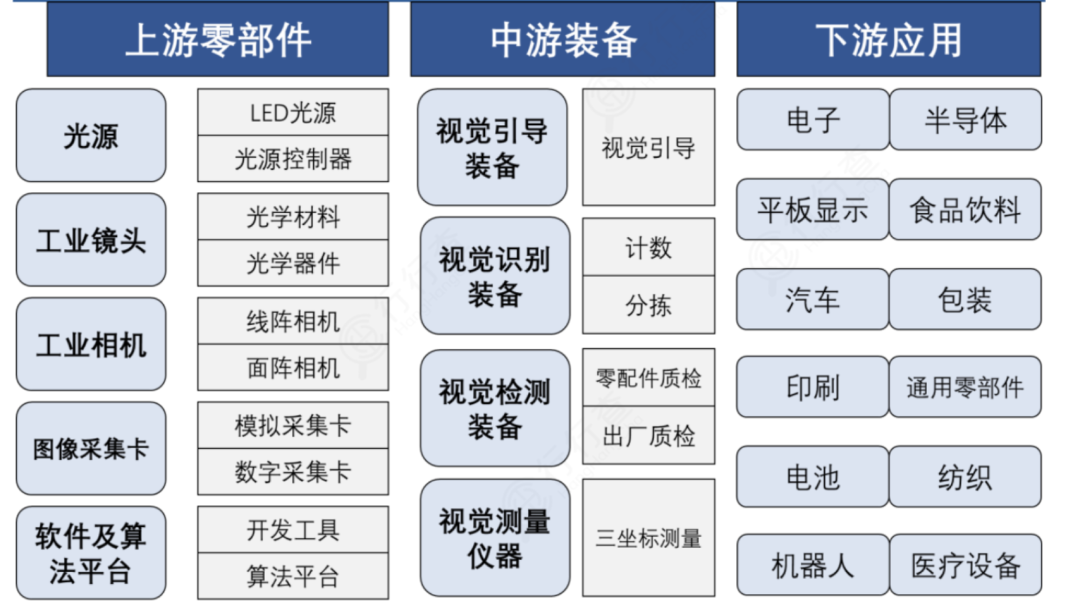

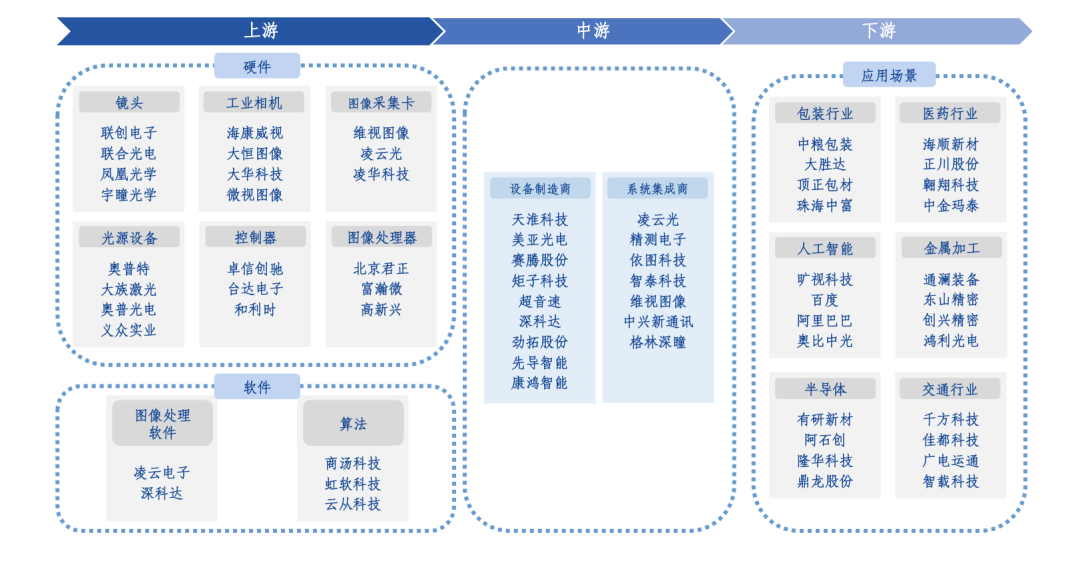

02. Machine vision industry chain

Machine vision can be divided into upstream (hardware, algorithm software), midstream (visual system, visual equipment integration), and downstream terminal applications.

The industry scope involved in the upstream is relatively broad, mainly including light sources, industrial lenses, industrial cameras, image acquisition cards, software and algorithm platforms, and other links; The midstream is the most crucial link in the machine vision industry chain, consisting of an integrated visual system and visual equipment; Downstream is the application field, widely used in various industries such as electronics, semiconductors, robotics, automobiles, and healthcare.

Source: White Paper on the Development of China's Industrial Machine Vision Industry

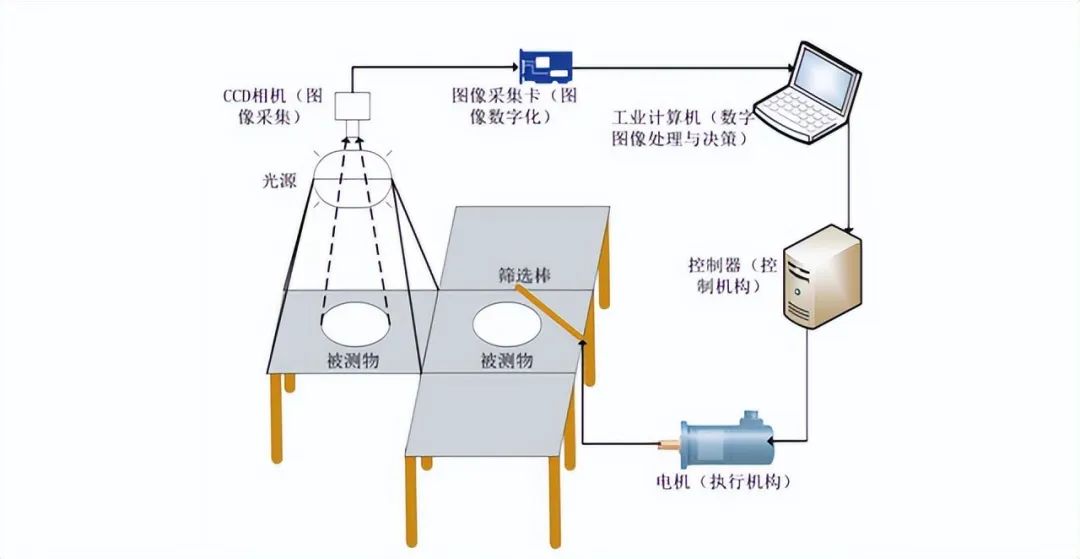

In a typical machine vision system, the light source and its controller, lens, camera, and other hardware components are responsible for imaging. The visual control system is responsible for processing and analyzing the imaging results, and outputting the analysis results to other executing mechanisms of the intelligent device.

The machine vision application system includes image capture, light source system, image digitization module, digital image processing module, intelligent judgment and decision-making module, and mechanical control execution module.

Light source and light source controller

The light source controller is used in combination with the light source. The light source controller supplies power to the light source and controls the lighting status (on/off), brightness, flicker, etc. of the light source.

The quality of a light source depends on its contrast, brightness, and sensitivity to positional changes. The machine vision industry mainly uses LED light source products.

At present, there is no universal machine vision lighting equipment, and personalized solutions are available for each specific application instance to achieve the best results.

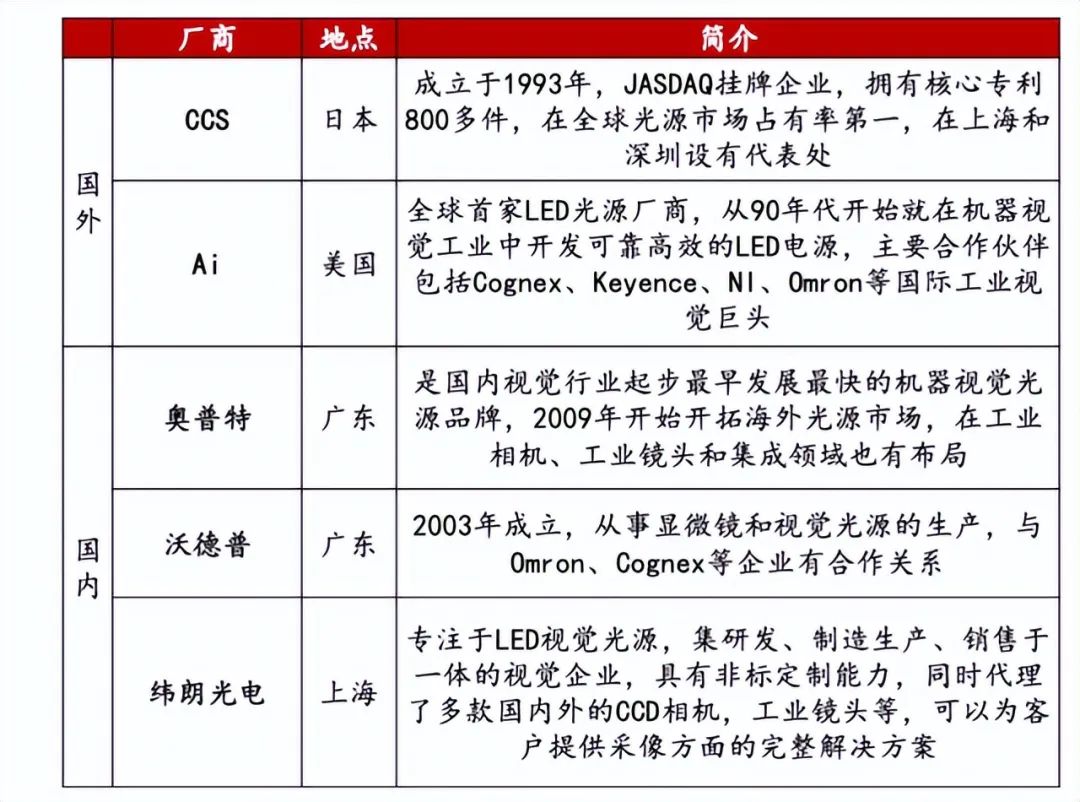

The high-end market of the light source industry is dominated by foreign companies such as CCS and AI, with a localization rate of over 90% in the mid to low end market. The degree of localization is high, and competition is relatively fierce.

Among domestic manufacturers, Optoelectronics is the company with the largest market share, and its main participating manufacturers include Waldorf and Weilang Optoelectronics, Daizu Laser, Yizhong Industry, etc.

Main domestic and foreign light source enterprises:

Industrial lens

The lens is equivalent to the lens of the human eye and serves as the starting point for machine vision to capture and transmit information about the subject. The lens used is an industrial grade lens. It requires smaller optical distortion, sufficiently high optical resolution, and rich spectral response selection to meet the application needs of different visual systems in different scenarios.

In terms of market structure, foreign enterprises have a higher market share in the high-end market, and domestic enterprises mainly promote cost-effectiveness. Currently, the localization rate in the mid to low end market is nearly 80%.

The main manufacturers in the industrial lens sector include Dongzheng Optics, Mutengguang, Pumis, as well as Lianchuang Electronics, United Optoelectronics, Phoenix Optics, and Yutong Optics.

Industrial cameras

A camera is an image acquisition unit in machine vision, equivalent to the retina of the human eye, which converts light signals into electrical signals.

Through the optical focusing of the lens on the image plane, images are generated, and after image acquisition, analog or digital signals are output. These signals are reconstructed into grayscale or color matrix images in the visual control system.

Industrial cameras are mainly imported from Europe and America, and domestic brands are gradually replacing them with imports from the low-end market.

At present, OPT, Hikvision Robotics (a subsidiary of Hikvision), Daheng Imaging, and Huarui Technology (a subsidiary of Dahua Group) all have industrial camera production capabilities.

Image processing software and algorithm platform

In machine vision systems, software and systems are the core, which can bring higher product premiums to the entire solution.

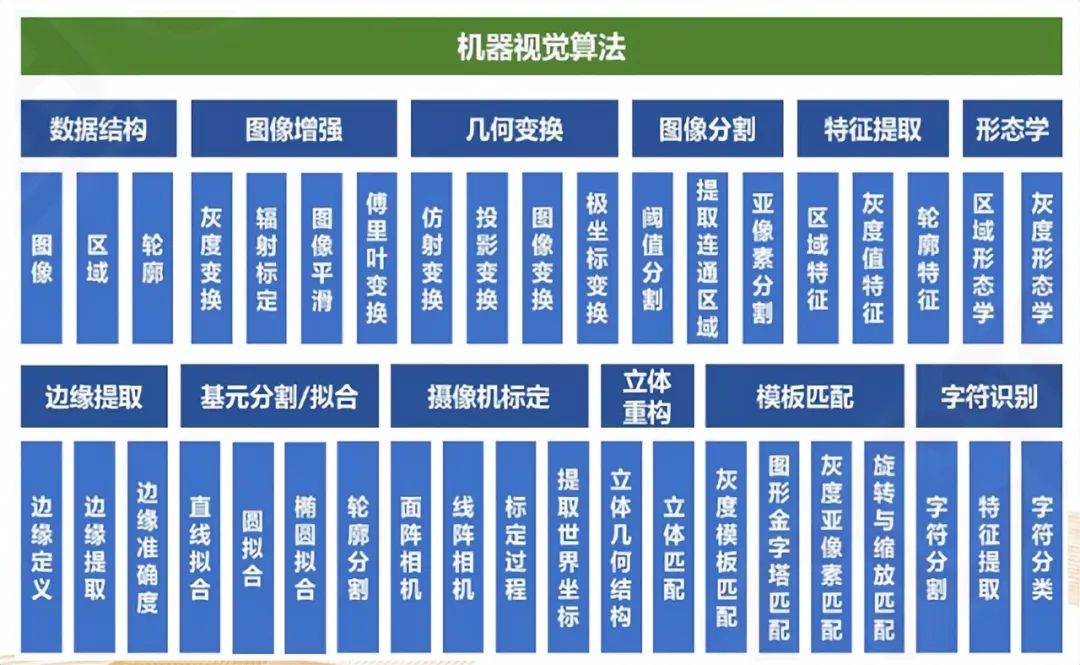

There are two main types of machine vision development tools, one is a toolkit containing multiple processing algorithms, and the other is application software specifically designed to implement a specific type of work.

The difficulty of the underlying algorithms is enormous, with foreign companies almost monopolizing the underlying algorithms, and local manufacturers actively breaking through. Currently, only a few domestic enterprises have self-developed algorithm libraries.

Representative domestic software and algorithm manufacturers include Lingyunguang, Shenkeda, Shangtang Technology, Hongruan Technology, and Yuncong Technology.

Manufacturers of image capture cards and image processors include Weishi Image, Lingyunguang, Linghua Technology, Beijing Junzheng, Fuhanwei, Gaoxinxing, and others.

Machine vision equipment and integration

Visual equipment is composed of automated equipment added to the visual system.

In addition to independent research and development, production, and sales of standardized machine vision core components, machine vision manufacturers also deeply integrate downstream practical scenarios and provide complete systems in a holistic solution model.

Domestic manufacturers are developing rapidly on the integration side, especially in some areas where foreign investment has not yet laid out, or in non-standard automation fields such as 3C.

At present, domestic integration manufacturers only have limited profit margins for secondary development. After completing a good layout in a certain industry downstream, they are expected to gradually expand to the upstream lower level development and import core software and hardware as substitutes.

The mainstream suppliers of domestic machine vision equipment include Tianzhun Technology, Lingyunguang, Optoelectronics, Juzi Technology, Meiya Optoelectronics, Jingce Electronics, Saiteng Co., Ltd., Obi Zhongguang, Jintuo Co., Ltd., Pioneer Intelligence, Kanghong Intelligence, etc.

The main layout providers of system integrators include Lingyunguang, Jingce Electronics, Yitu Technology, Zhitai Technology, Weishi Imaging, Green Deep Eye, etc.

From the perspective of the global market structure of machine vision, domestic brands are competitive in the mid to low-end market, while the high-end market is still dominated by overseas brands.

Keyence and Cognex dominate the majority of the global market share, with a combined global market share of over 50%.

And both major international giants have strong profitability, which also reflects the high industry barriers of machine vision, mainly due to the two characteristics of "technology intensive" and "process intensive" in the machine vision industry.

Since the introduction of machine vision systems in China in 1998, the number of enterprises participating in the development of the machine vision industry has been increasing year by year.

According to data from Qichacha, from 2010 to 2019, the number of new industry related enterprises increased year by year. By 2019, the number of new machine vision enterprises had reached 819, reaching the peak of new value-added in recent years.

Since 2020, due to the impact of the epidemic and the increase in industry concentration, the number of new enterprises added each year has gradually slowed down. In 2021, a total of 278 new machine vision related enterprises were added, and the market pattern is still relatively scattered.

Machine vision industry chain and some representative manufacturers:

Source: Great Wall Securities

Machine vision is a key component of intelligent manufacturing equipment. Currently, 90% of manufacturing enterprises have automated production lines, but only 40% achieve digital management, 5% connect factory data, and 1% use intelligent technology. In most scenarios, recognition and detection still rely on manual labor or simple equipment.

According to data from Cognex, it is estimated that out of 360 million manufacturing workers worldwide, there are approximately 35 million visual quality inspectors, and the annual labor costs incurred solely due to visual inspection worldwide exceed $300 billion.

The savings in labor costs are only one part of the value added by machine vision to downstream. If we consider the improvement of product quality and consistency, digital production, and the incremental application of machine vision in high-precision and complex scenarios.

Overall, the proportion of China's industrial added value to the global market is continuously increasing. In the future, driven by various rapidly growing industries such as autonomous driving, medical imaging, and industrial robots, it is expected to boost the demand for the machine vision industry, and the industry market prospects are broad.